My Projects

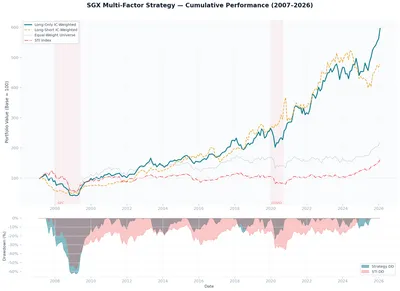

Multi-Factor Equity Strategy — SGX

Quantitative Research

Systematic multi-factor long-short equity on SGX with a point-in-time survivorship correction (NTU FYP).

Factor InvestingQuantPython

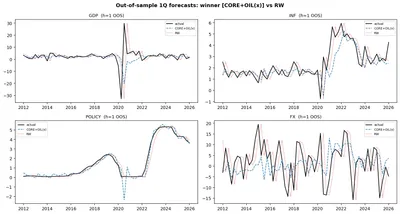

Macro Forecasting Horse Race

Quantitative Research

An honest out-of-sample horse race across five macro forecasting model classes.

EconometricsForecastingBayesian

Volatility & Systematic Strategy Lab

Quantitative Research

A multi-strategy lab around the volatility risk premium, with a Black-76 options engine.

VolatilityOptionsBacktesting

Congressional-Trade Alpha — An Event Study

Machine Learning / Quant Research

An event study on whether copying congressional trades is an edge (it isn't).

Event StudyAlt DataPython

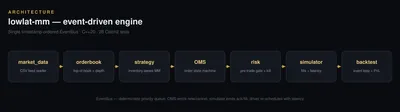

Low-Latency Market-Making Engine

Systems / C++

A C++20 event-driven market-making and execution engine.

C++Market MakingLow Latency