Macro Forecasting Horse Race

About this project

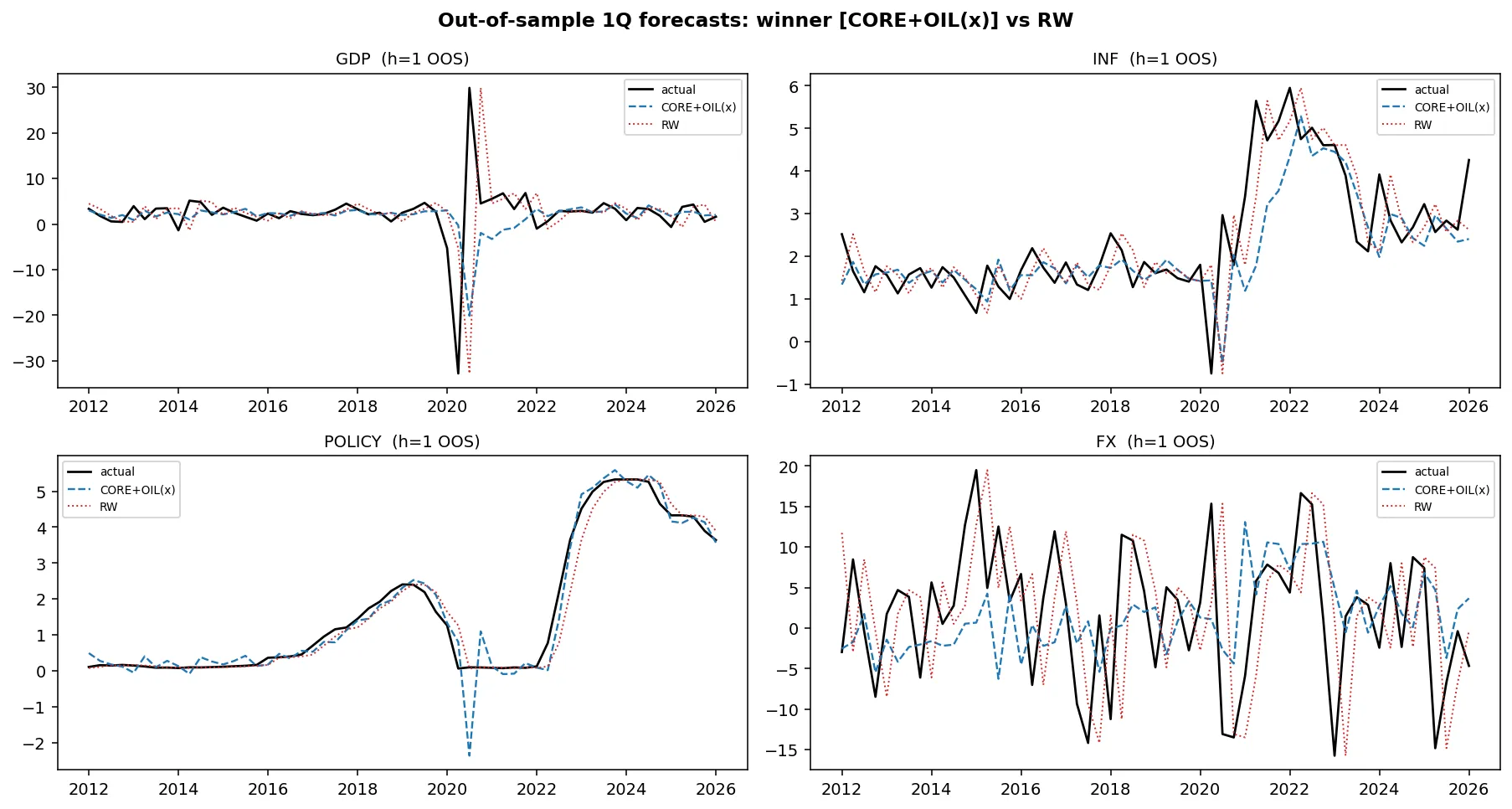

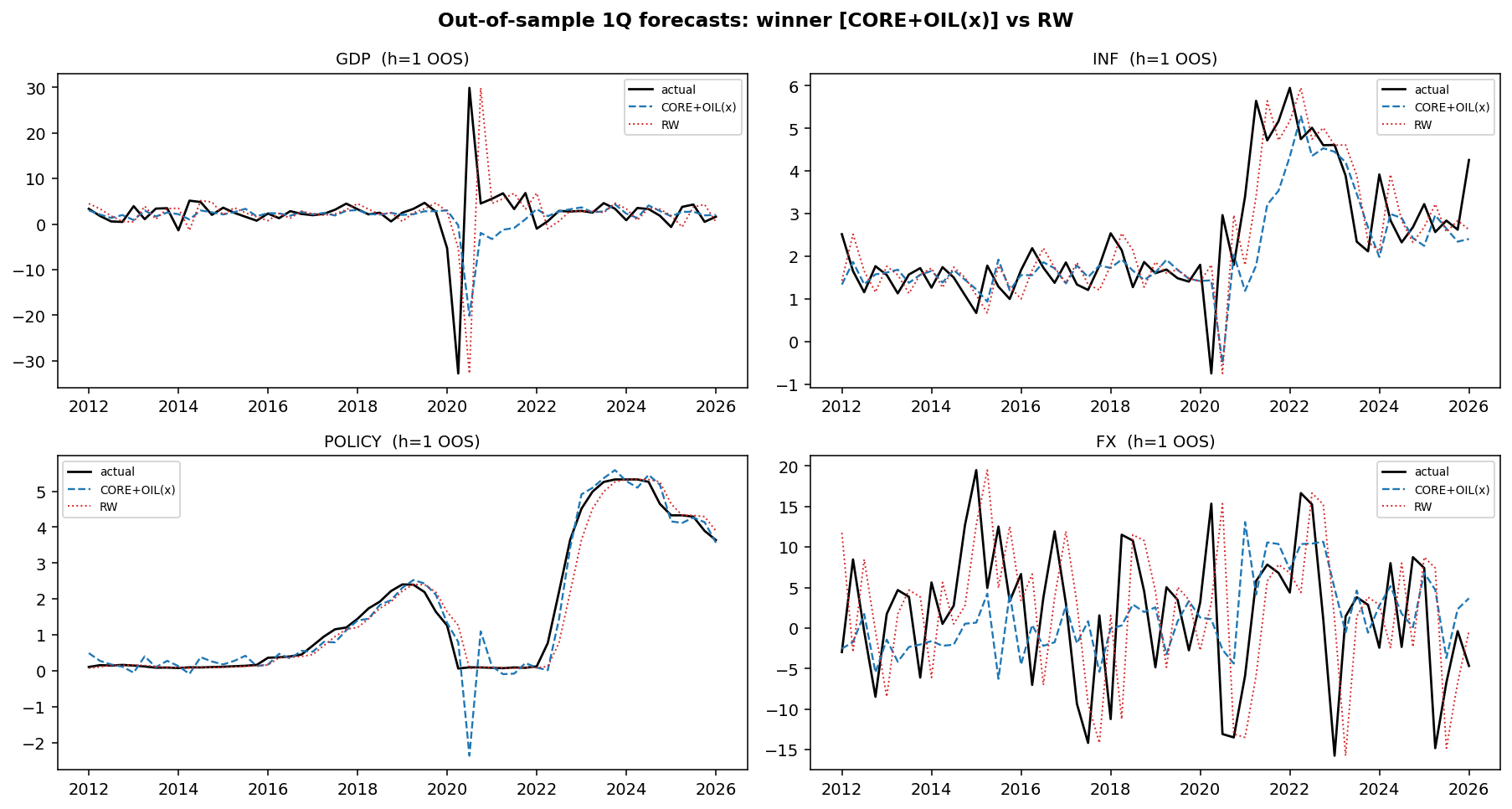

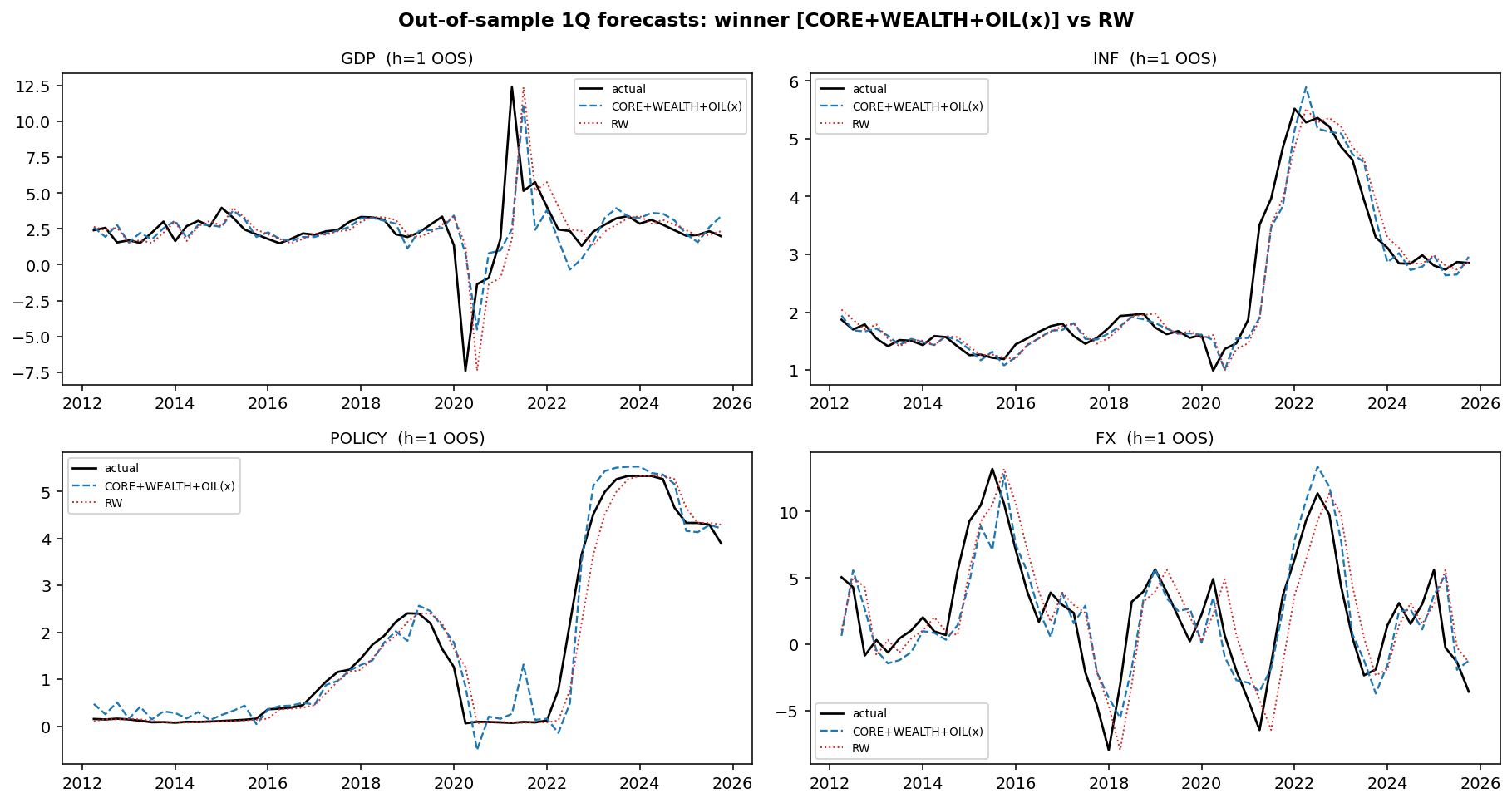

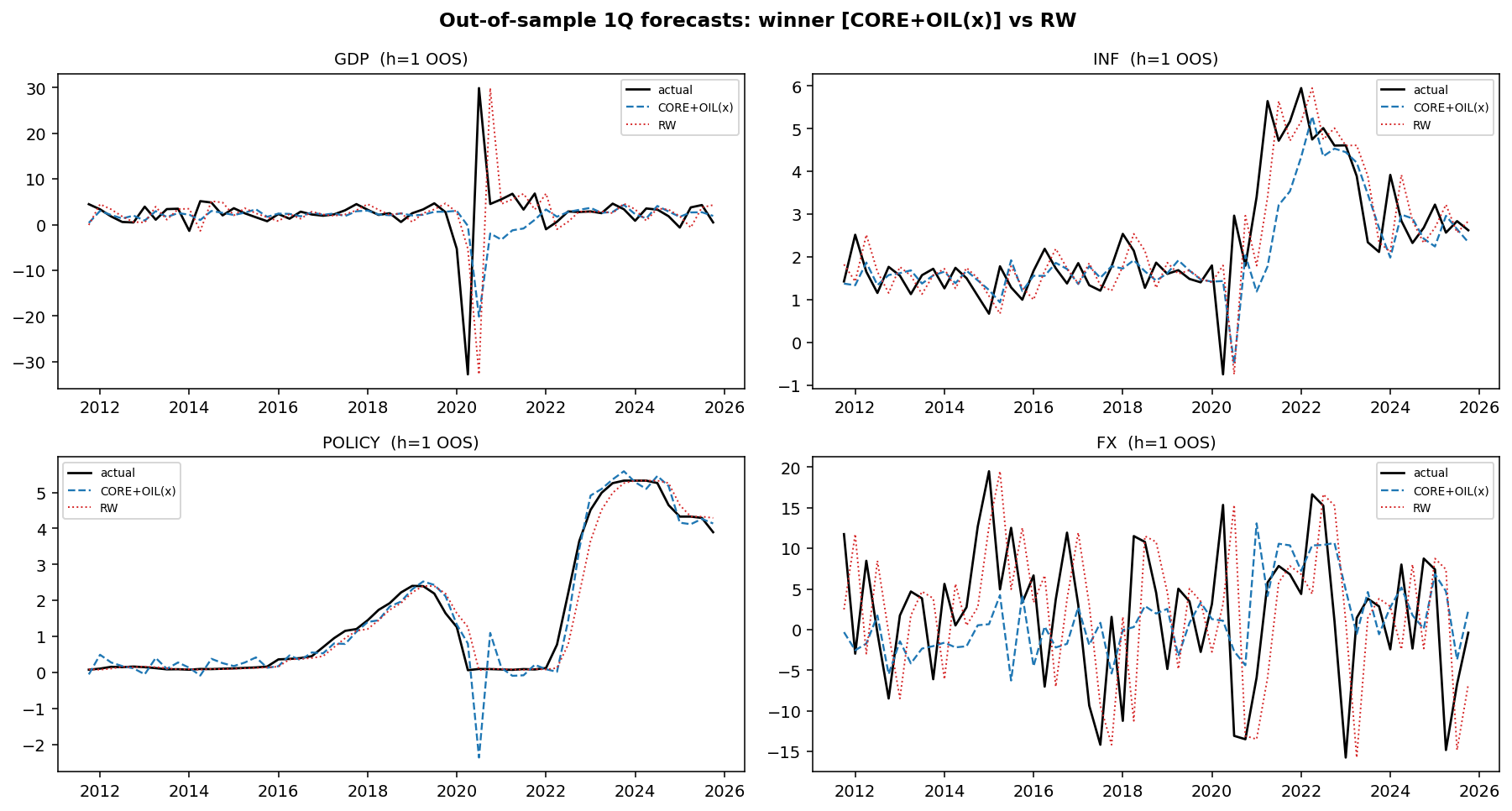

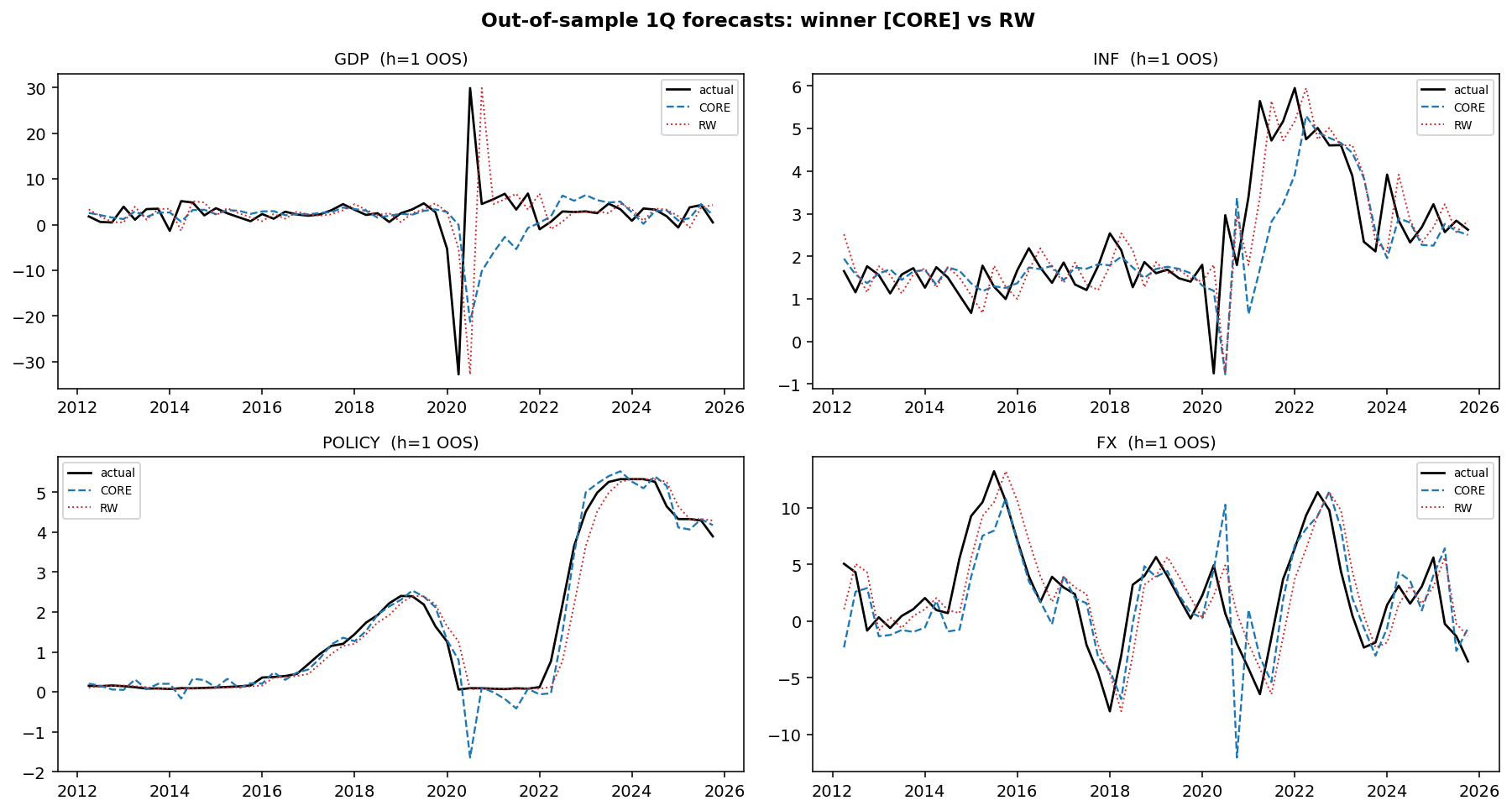

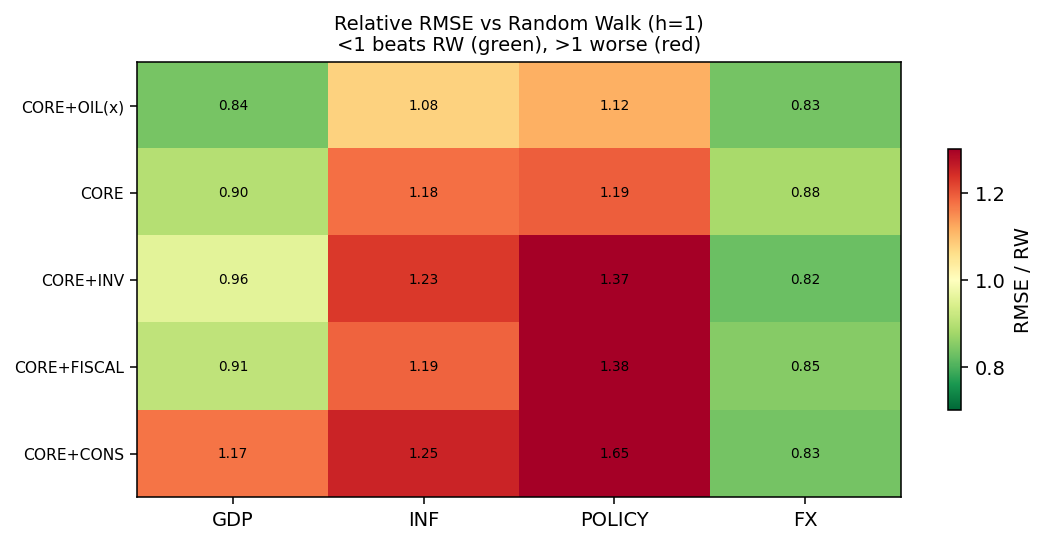

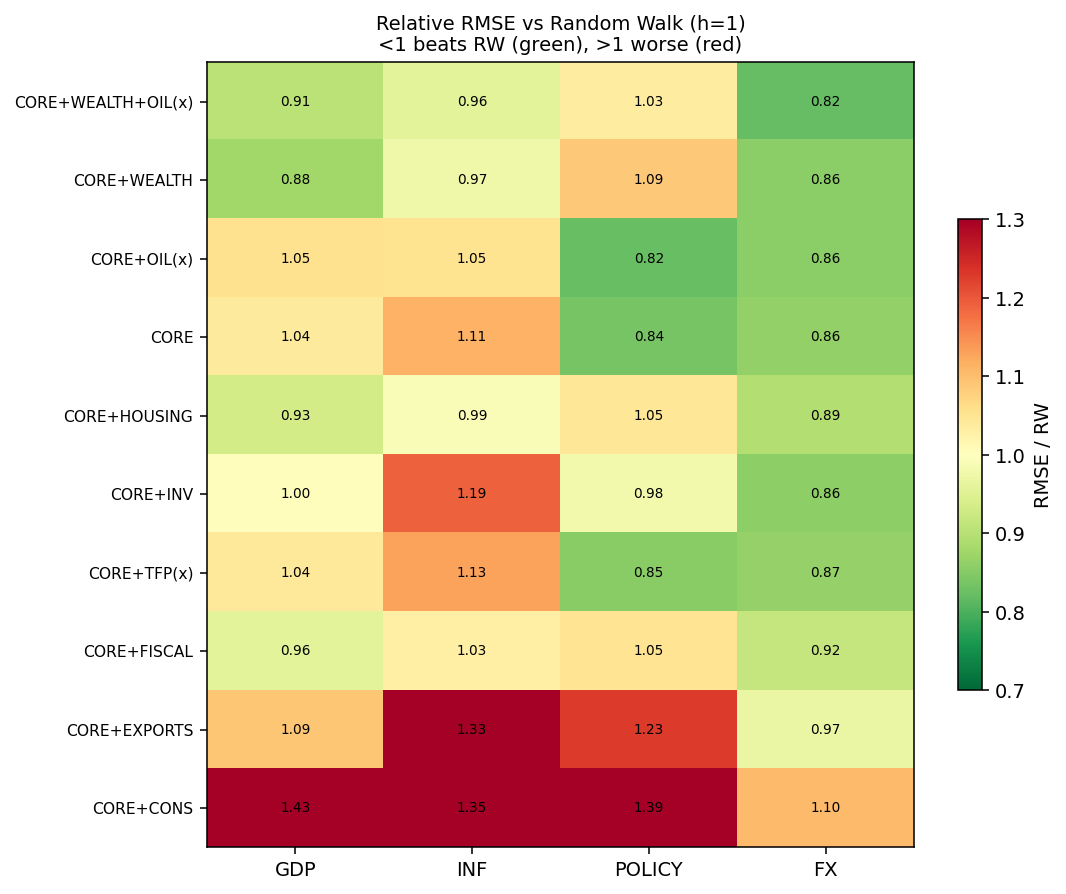

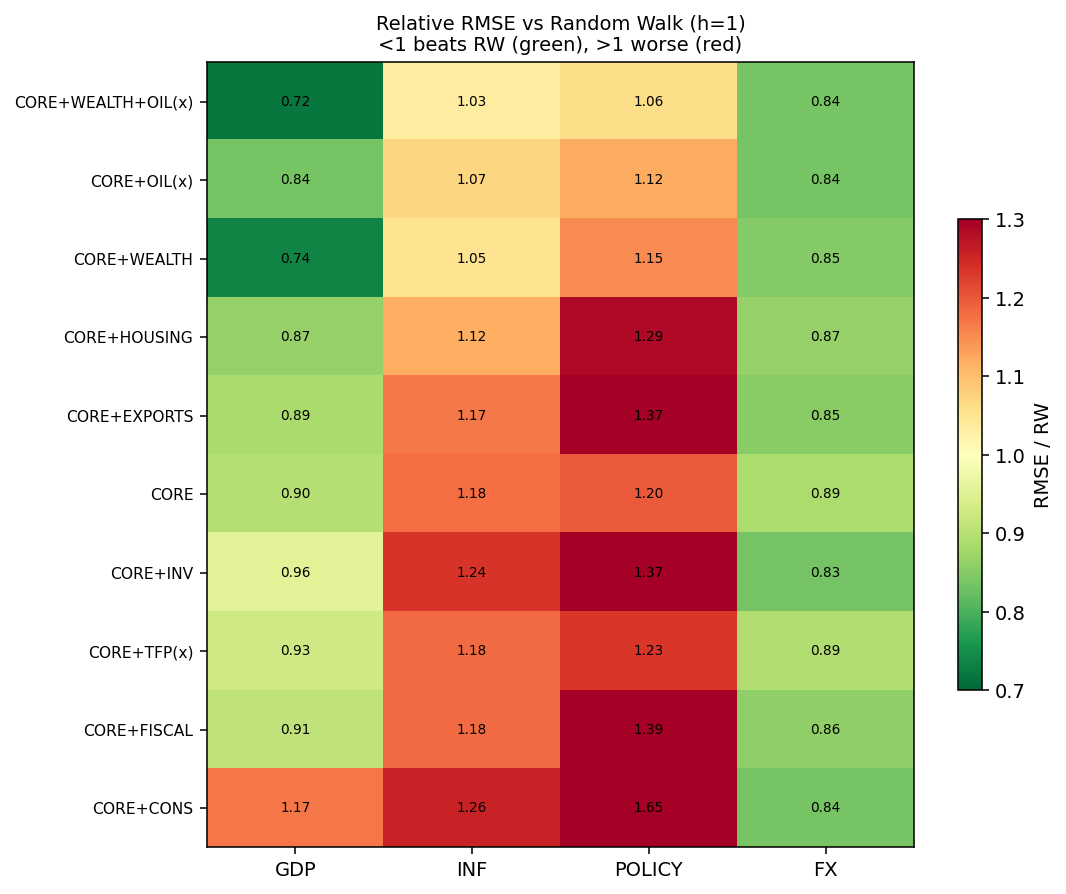

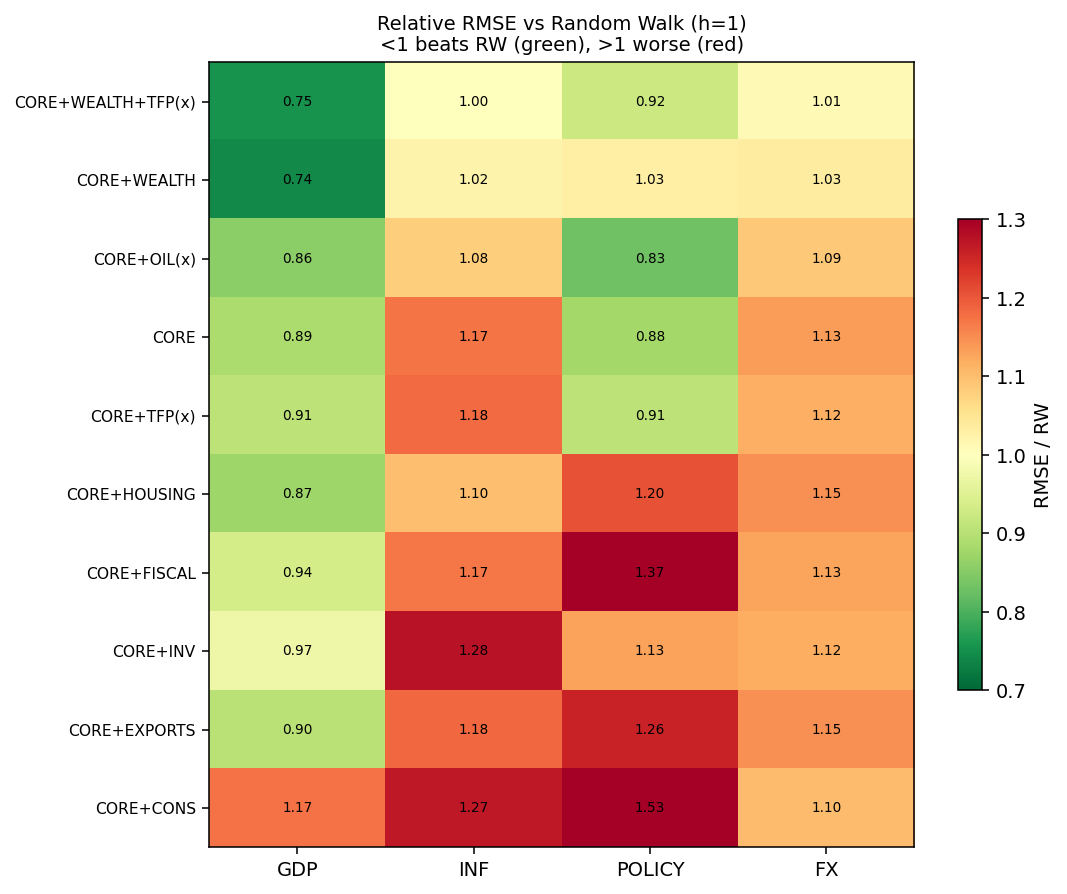

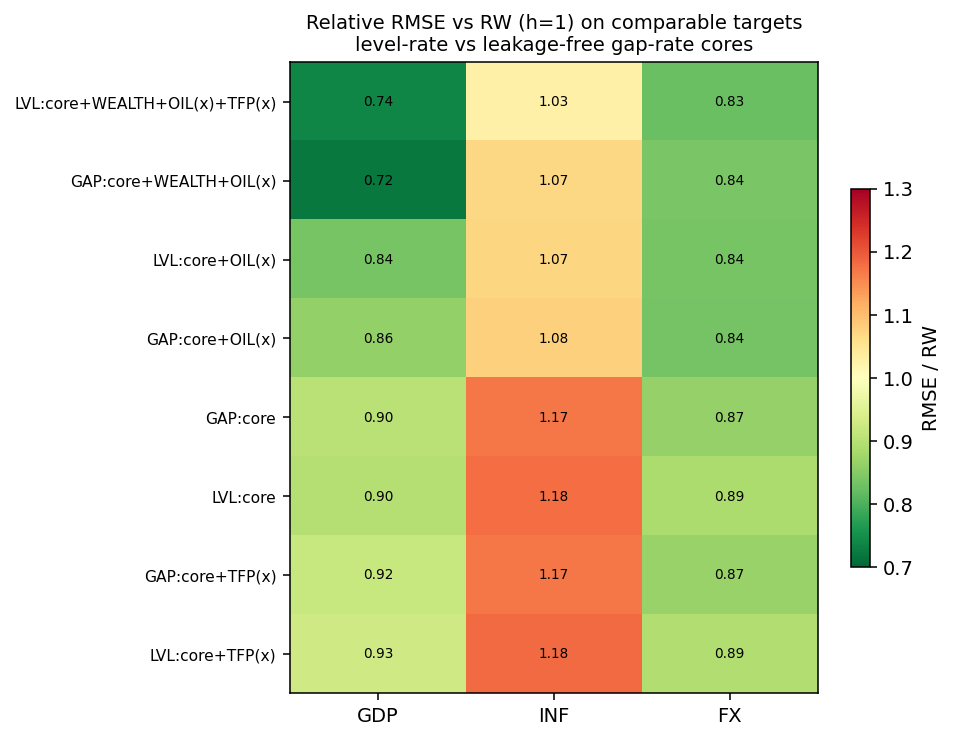

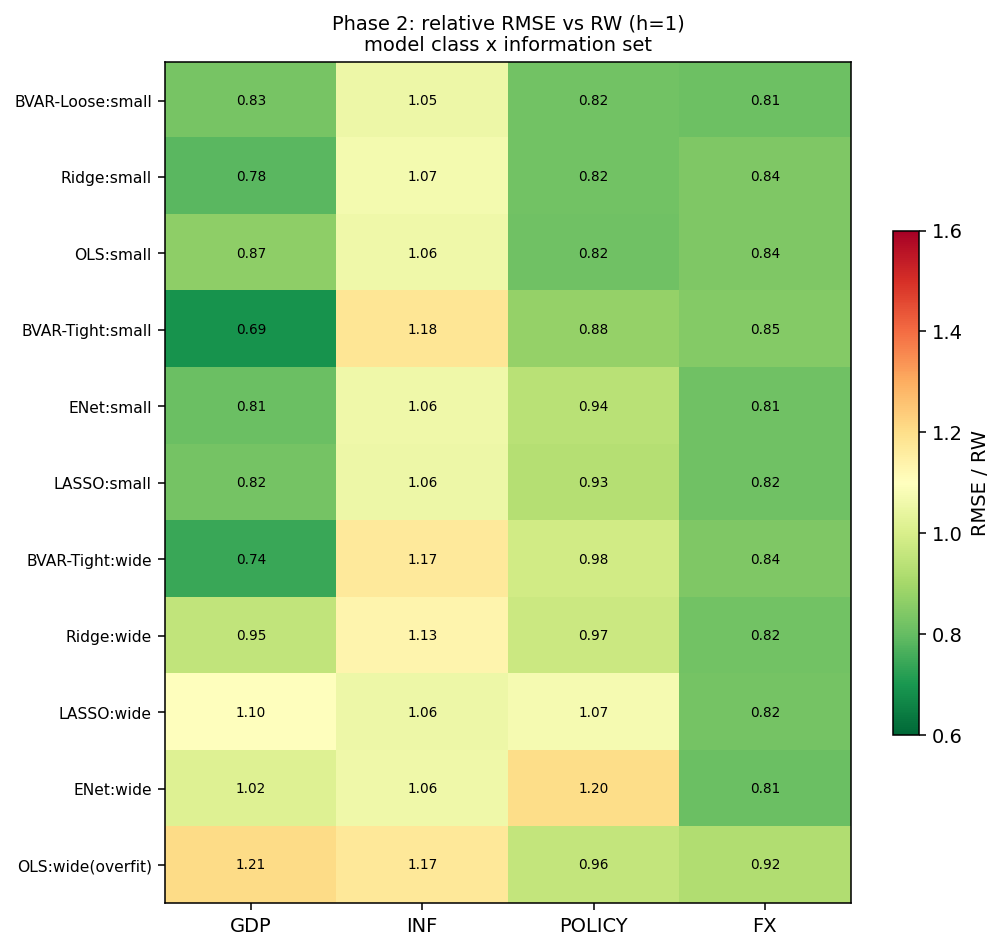

A reproducible out-of-sample horse race across five model classes — random walk, AR, VAR, Bayesian VAR, and shrinkage methods — over 128 quarters of US macro data. Judged honestly with Clark-West, Diebold-Mariano, and the Model Confidence Set. The BVAR edges the naive benchmarks on most targets, but only the real exchange rate beats them significantly (DM p=0.026), and the random walk survives the Model Confidence Set everywhere. The finding is the restraint: macro variables are genuinely hard to forecast beyond no-change, and the framework refuses to overclaim it.

Challenges

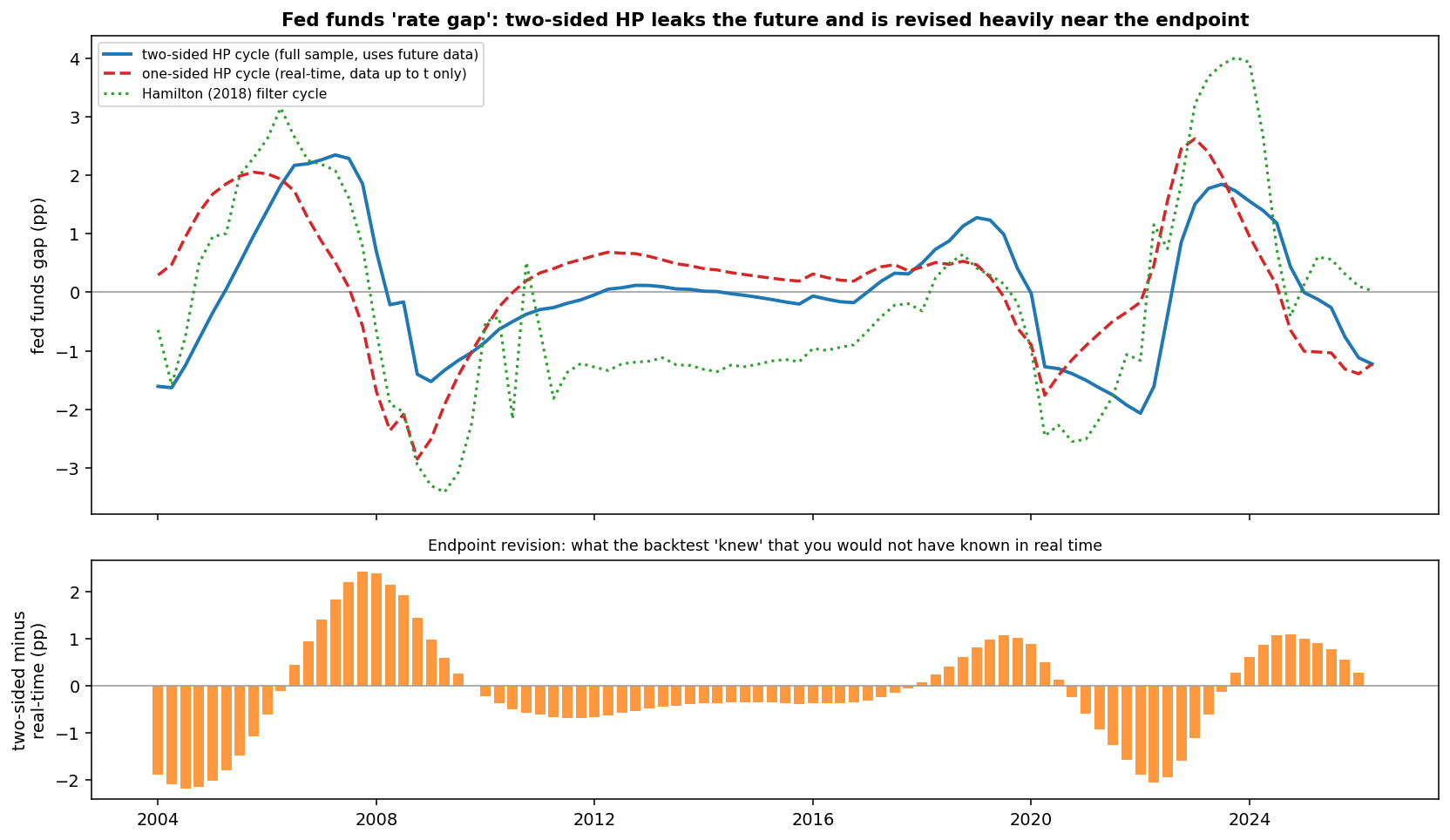

Implementing a leakage-safe walk-forward protocol, the Minnesota BVAR with a sum-of-coefficients prior, and the Model Confidence Set to guard against data-mining.

Learnings

Bayesian time-series, formal forecast evaluation, and that an honest negative result is worth more than an overfit positive one.