Multi-Factor Equity Strategy — SGX

About this project

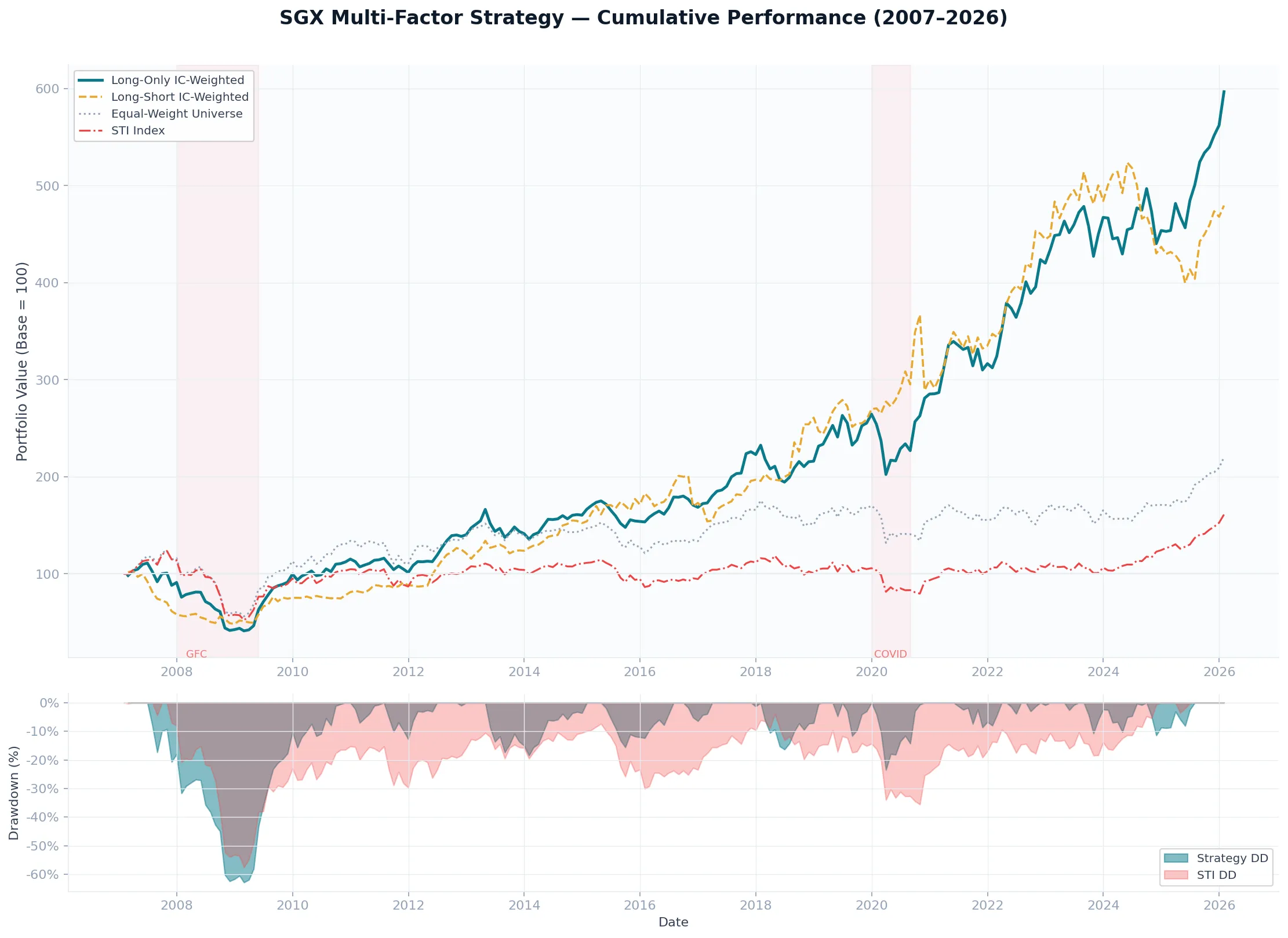

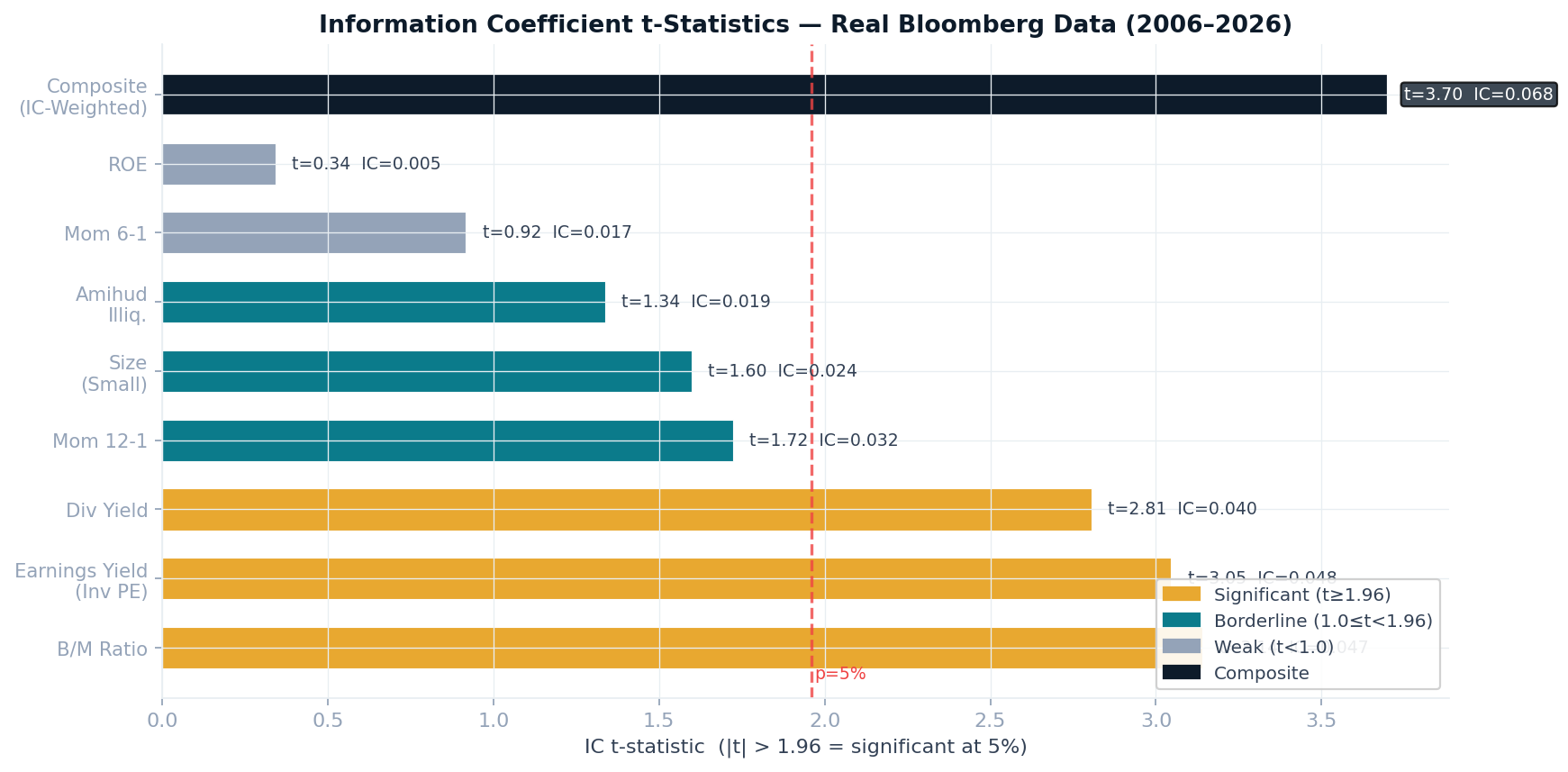

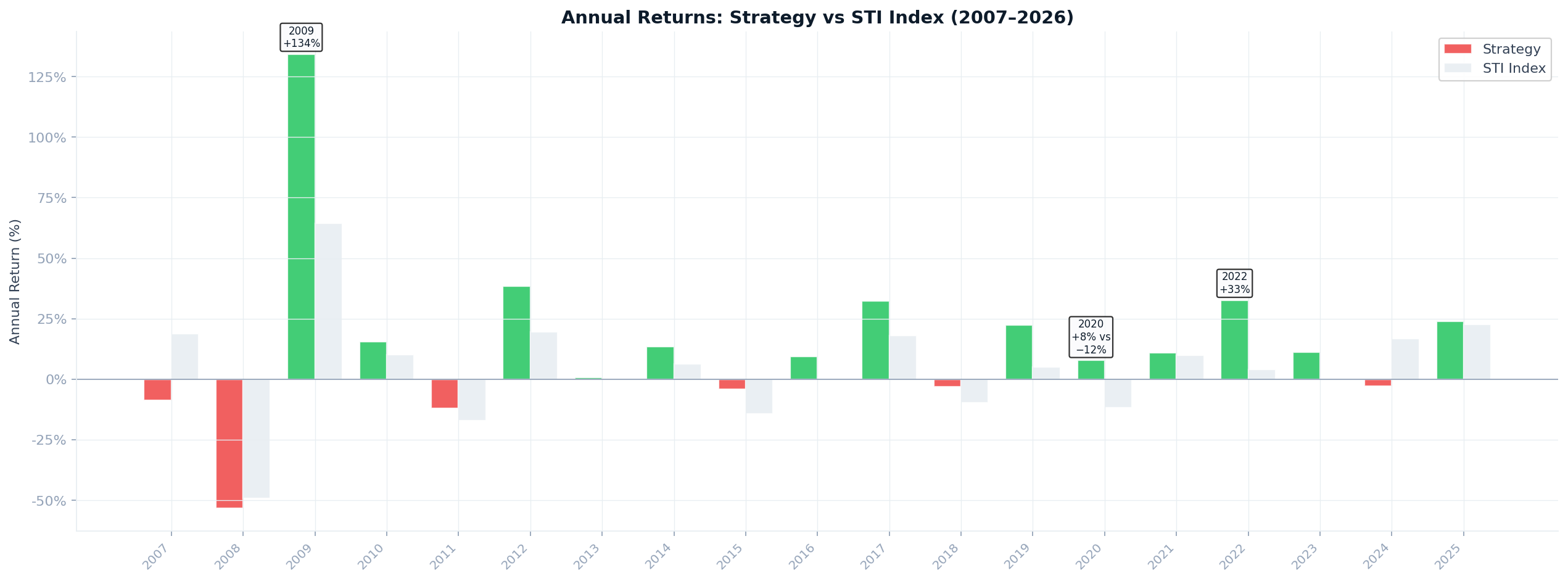

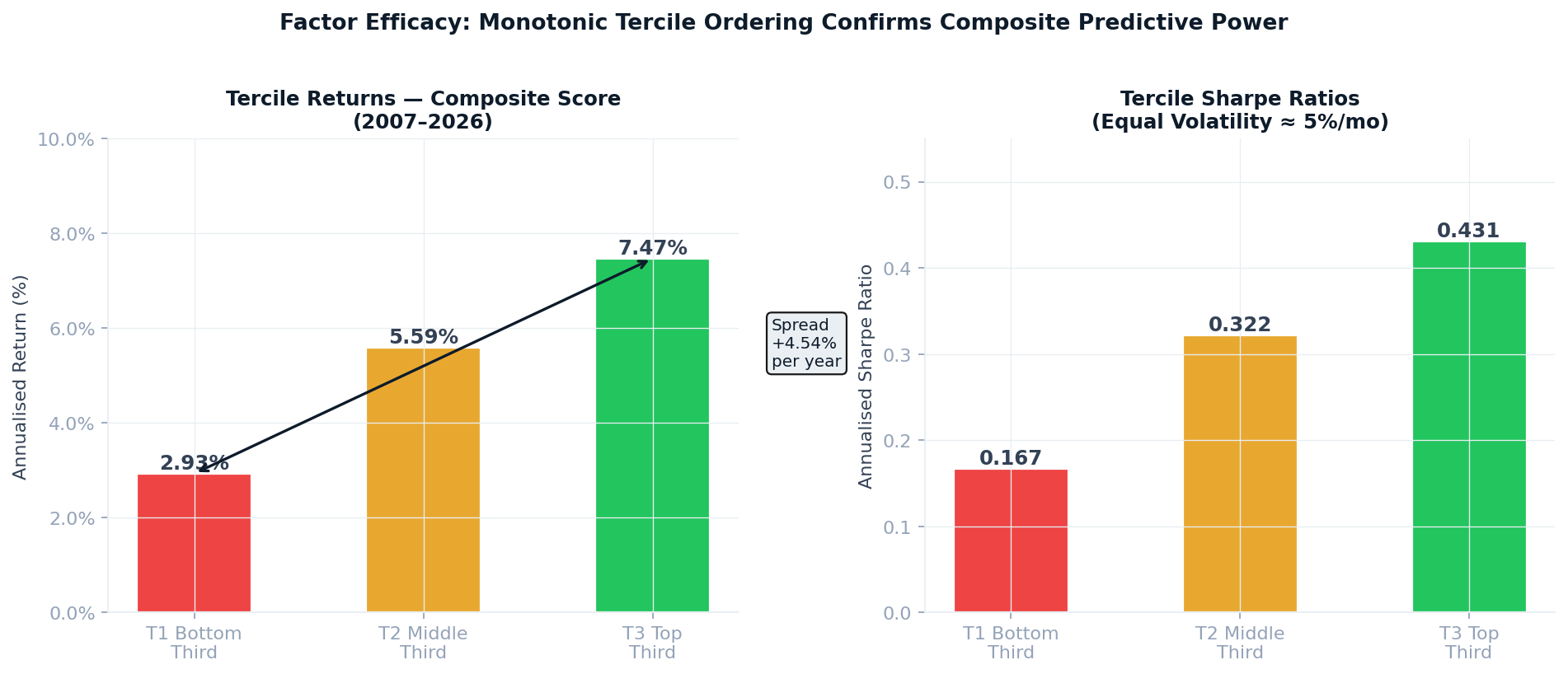

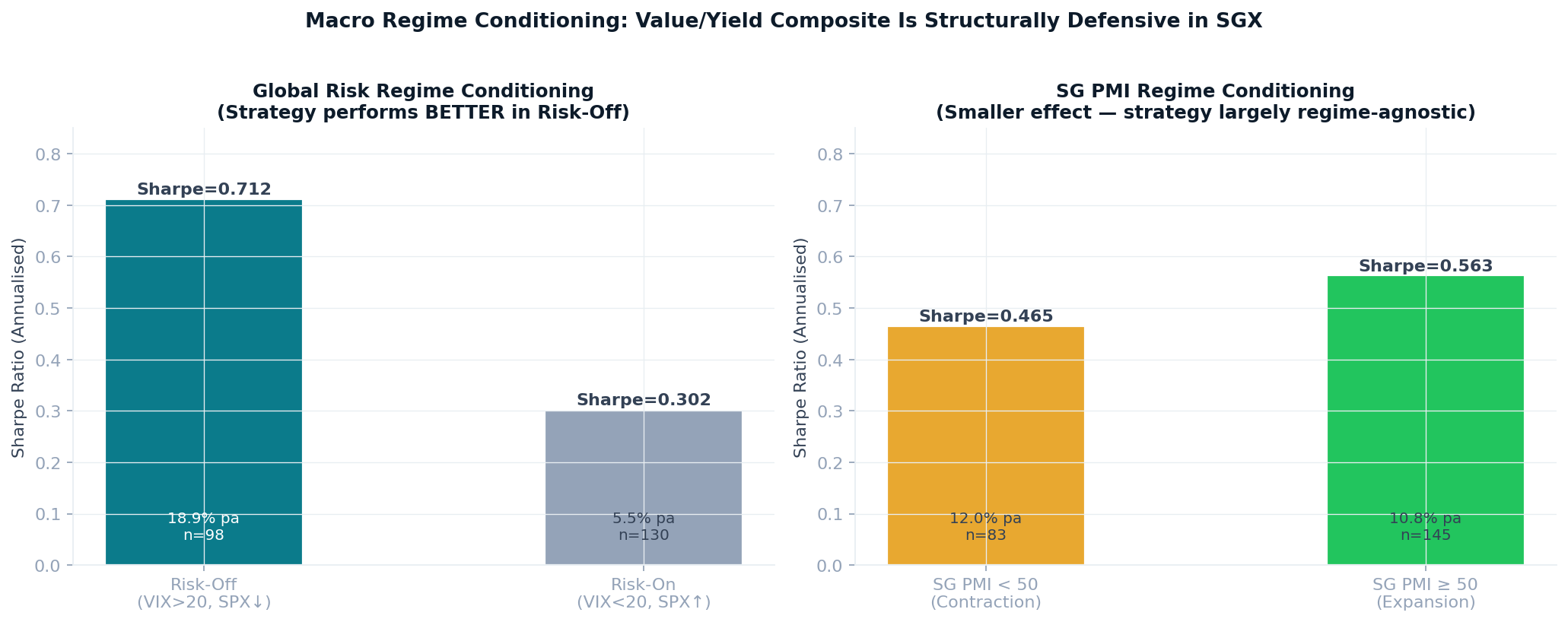

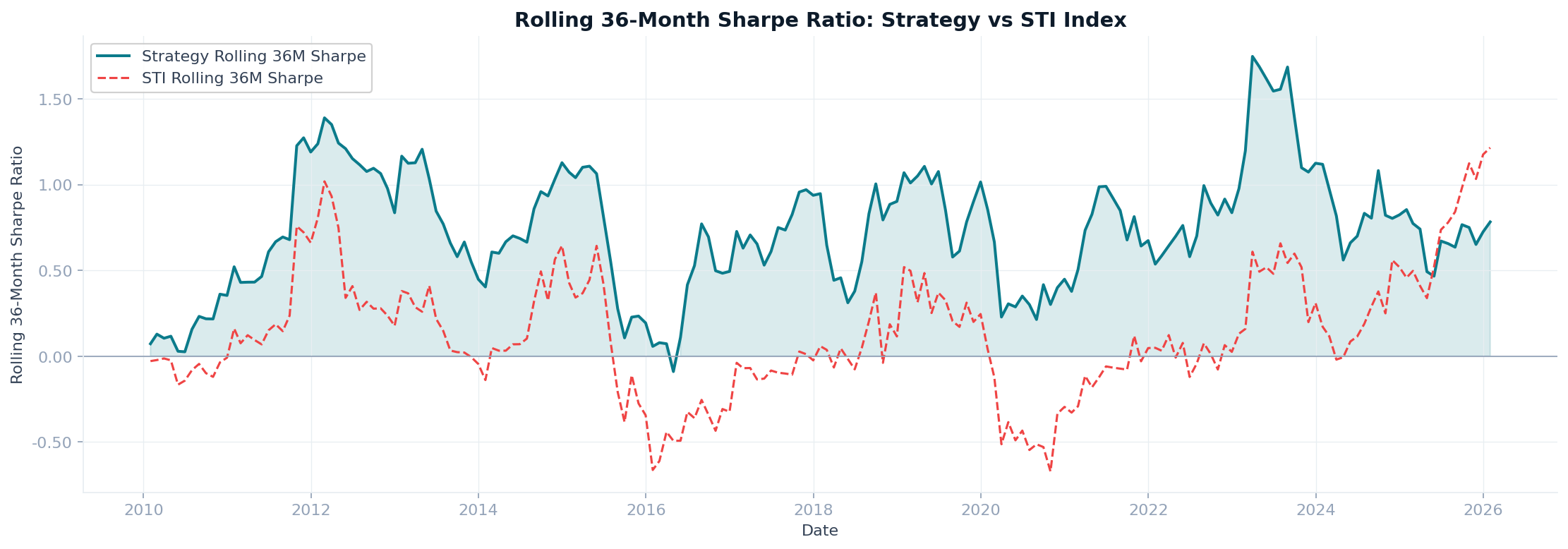

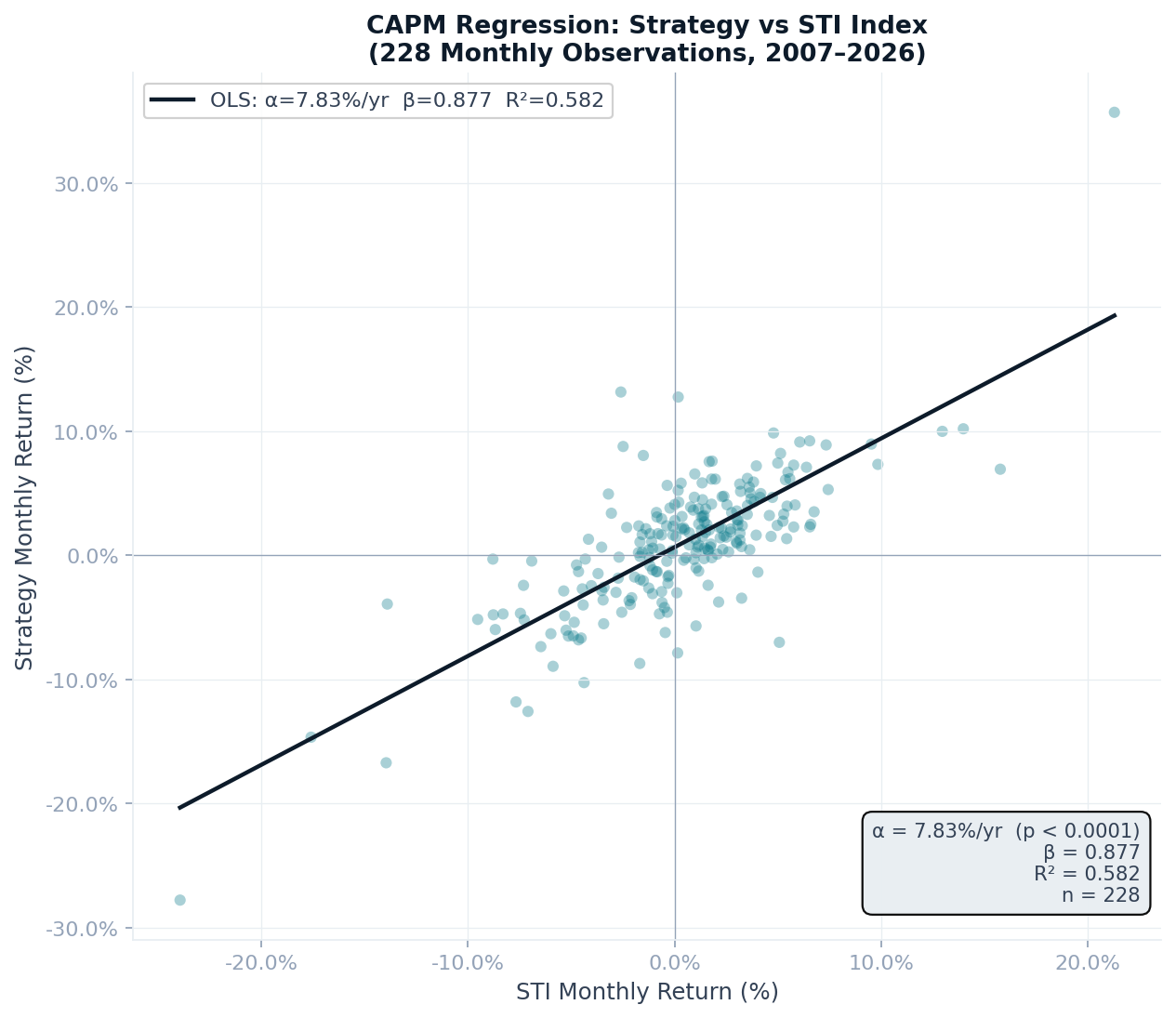

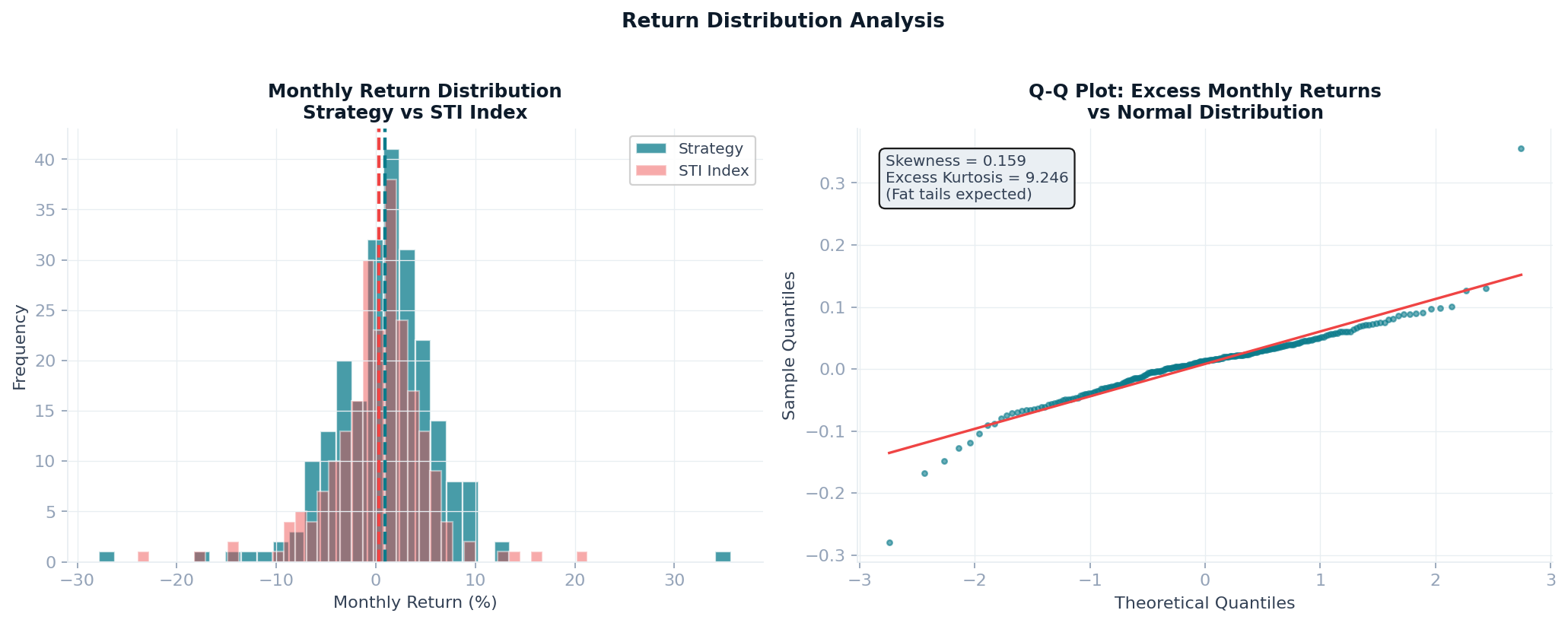

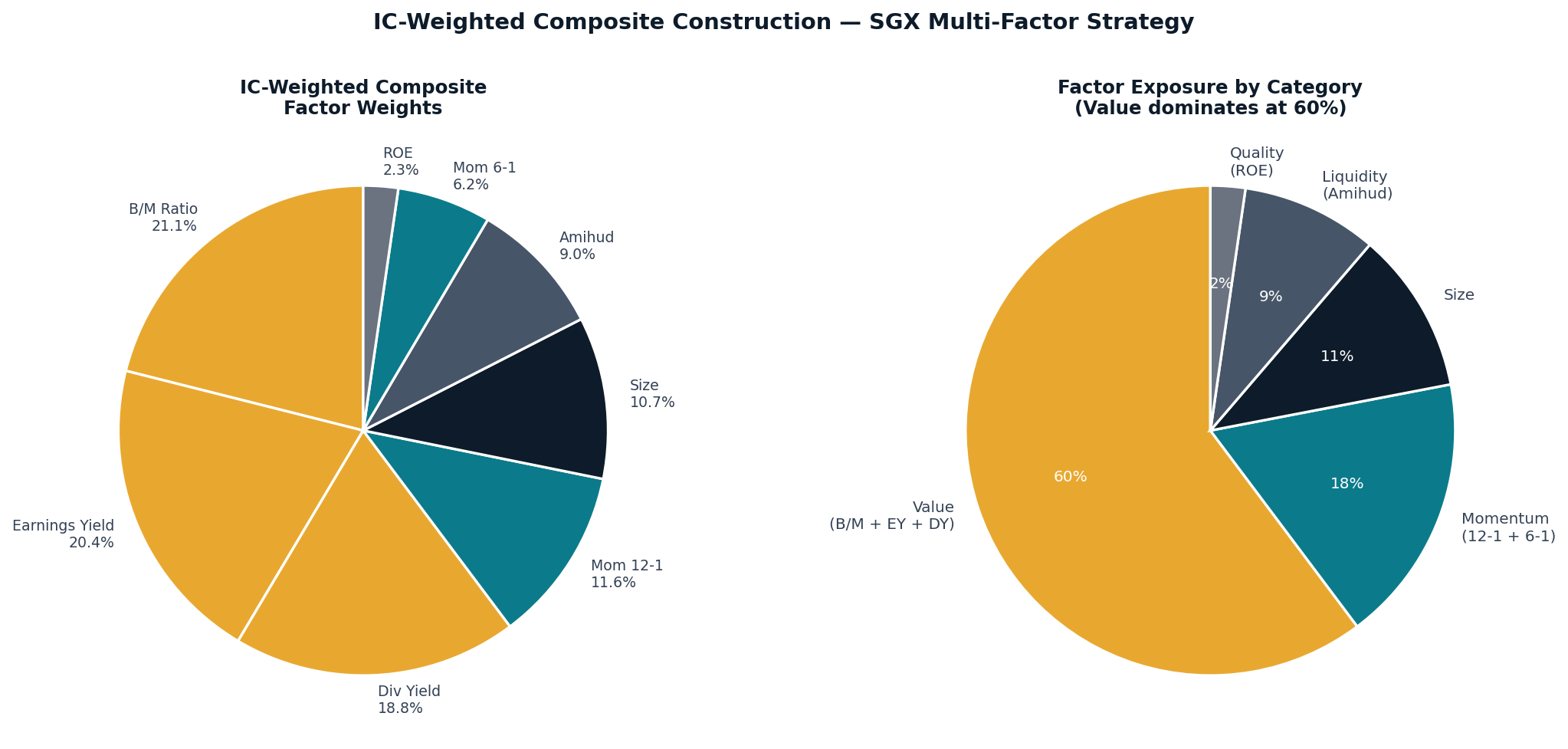

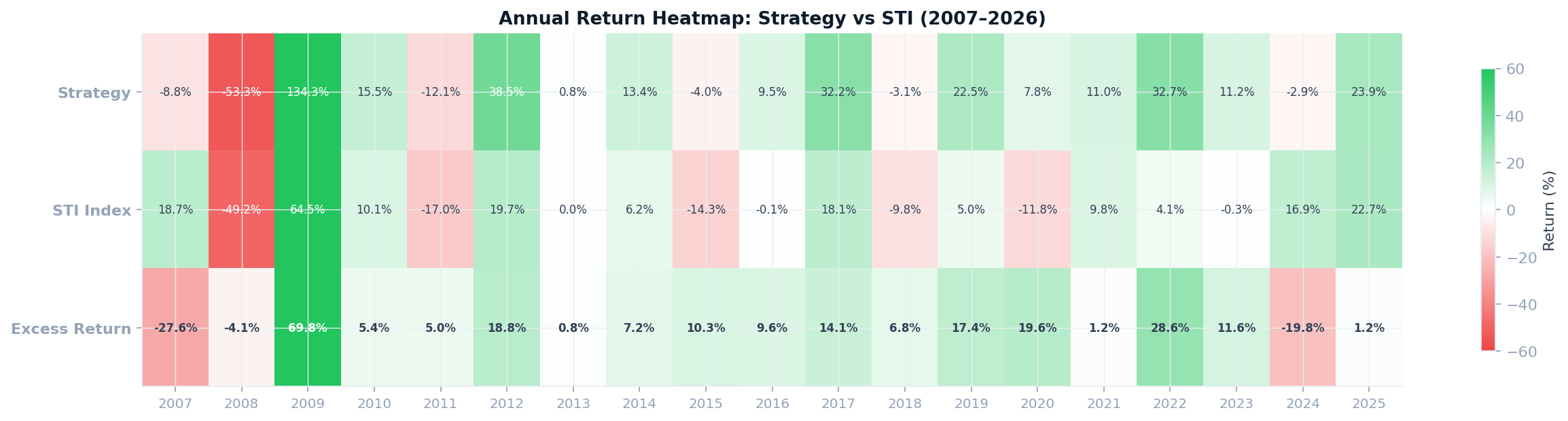

A systematic multi-factor long-short strategy on Singapore equities, built as my final-year project. Value, momentum, quality, size and liquidity signals combined into an IC-weighted composite, tested with Fama-MacBeth pricing, a regime overlay, and a point-in-time survivorship correction. The survivorship work is the core finding: rebuilding the universe to include delisted names cuts the long-only Sharpe from 0.98 to 0.61, a ~1.6%/yr survivorship premium the naive survivor-only universe hides. Composite factor IC 0.075 (t=5.05); value carries the signal, momentum and quality don't.

Challenges

Building point-in-time index membership to remove survivorship bias, handling delisted names, and aligning fundamentals with a 45-day reporting lag to avoid look-ahead.

Learnings

Factor construction and Fama-MacBeth testing, and how much measured performance is an artifact of survivorship if you don't correct for it.